As we get closer to the highly anticipated rate cuts from the Bank of Canada, everyone’s focus is on falling mortgage rates. However, mortgage lenders have been increasing their fixed rates, and it’s possible that they could increase even further.

This can sound strange to many. With so much talk about rates dropping, why is it that fixed mortgage rates are moving the other way?

Many believe that fixed mortgage rates move with the Bank of Canada rate. While they are related, they do not move together. Fixed mortgage rates are heavily influenced by bond yields, which can move in either direction at any time.

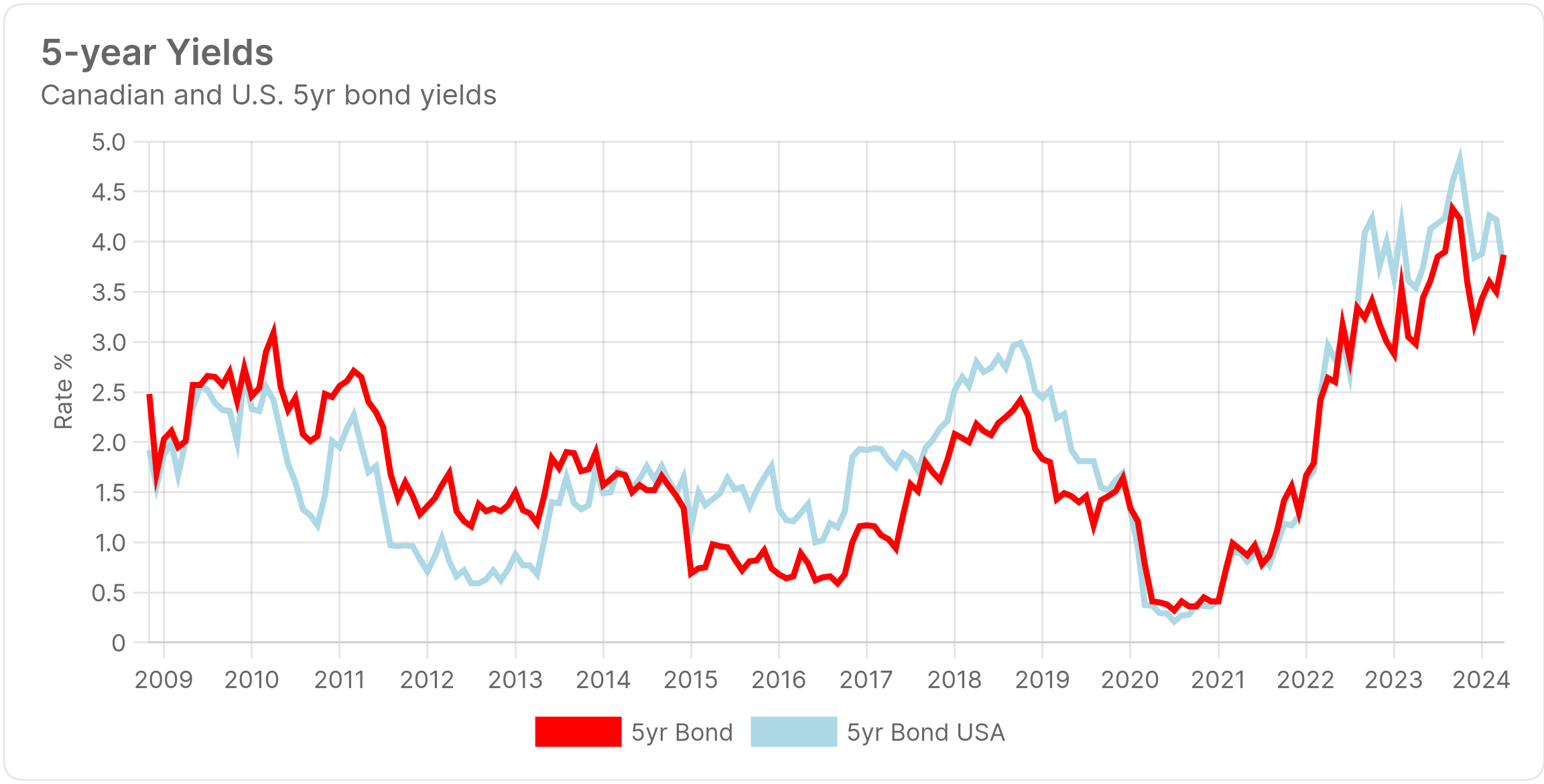

Canadian bond yields will generally follow those from the US as you can see in the chart below:

Source: MortgageLogic.news

Given that the US economy has been strong while unemployment remains low, they are struggling to bring inflation under control. This is what’s been driving their bond yields higher, which is bringing the Canadian yields with them.

The result?

Increases to fixed mortgage rates.

When are the Rate Cuts Expected?

If the US continues to struggle with inflation, then it’s likely that they’ll need to push out the timing of their first rate cut to later this year.

In Canada, our economy is worsening, unemployment is rising, and inflation is dropping nicely. This is exactly what the Bank of Canada wants to see. This led to inflation dropping into the 2% range, which nicely positions the Bank of Canada to cut their rate soon.

Just as the Canadian bond yields are closely tied to the US, so are the central bank rates. Canada will generally follow the US, but this is not always the case as you can see in the comparison chart below:

Source: MortgageLogic.news

While they are generally close, there are also times when Canada needs to do its own thing. As Canada’s inflation is in a much better position, the BoC is prepared to cut their rate sooner. They will not wait for the US, and if it seems like the time is right, they’ll cut their rate as expected.

The next scheduled rate announcement from the Bank of Canada will be on June 5th. The expectations for this date are mixed. Three of the big six banks have been forecasting a cut, while the other three are not expecting it to happen in the third quarter. You may as well flip a coin.

I discussed the forecasts from the big banks in detail in last week’s blog: Don’t Wait to Lock in a Mortgage Rate

US and Canadian Inflation Expectations and Their Influence on Mortgage Rates

There are two inflation reports expected prior to the June 5th rate announcement. The US will be releasing their next report on May 15th, with the Canadian report coming six days later on May 21st.

If the US report comes back with promising numbers, then I would expect bond yields to fall on both sides of the border. If it fails to meet expectations, then I would expect another upward spike in yields, putting further upward pressure on fixed rates.

If the Canadian inflation report comes in better than expected on May 21st, then this increases the chances that we’ll see a cut on June 5th. However, I personally think that the BoC will err on the side of caution and push their first cut out to their next announcement date on July 24th.

Time will tell, but the cuts are close either way!

Fixed and Variable Rate Spread Will Shrink

As the Bank of Canada starts dropping their rate, the spread between fixed and variable rates will begin to narrow. Yes, fixed mortgage rates are expected to drop, but not quite at the same pace as the Bank of Canada cuts. Eventually, variable rates will be lower than their fixed as they are in most markets.

Conclusion

Higher mortgage rates are frustrating for everyone. But we’re getting closer to the cuts. While upward pressure continues on fixed rates, this will eventually reverse, and fixed rates will start to fall as expected.

While the exact timing of the first rate cut from the Bank of Canada is uncertain, if we don’t see a cut in June, then chances are strong that we’ll see it in July. The cuts are coming soon, it’s just a matter of when they start.

We’re expecting to see the Bank of Canada drop their rate by 0.75% to 1.00% before the end of 2024, with another 0.75% to 1.75% by the end of 2025, depending on which forecast you follow. Further cuts in 2026 are also likely.

Fixed mortgage rates will come down, but as I’ve said on multiple occasions, it’s not expected for them to drop in a straight line. It was always expected to be some bumps along the way.

As upward pressure on fixed mortgage rates continues, anyone with a purchase closing or a mortgage renewal coming up within the next 120 days should lock in a rate asap to ensure you’re protected. We’re very serious about saving you as much money as possible. Contact us to find out the lowest rate you’ll be eligible for.

Other relevant blogs:

Are 3 Year Fixed Rates Still Your Best Bet?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment